Water From Thin Air Is Fascinating. Investing in It Is Much Harder.

- Michael Shmilov

- Apr 8

- 6 min read

Why this topic matters

For a long time, “water from air” sounded to me like one of those ideas that are easy to love in a headline and much harder to trust as a business. But the need behind it is real. Water stress is growing. Climate patterns are becoming less predictable. Populations are growing. Industrial demand keeps rising. So even if atmospheric water harvesting never replaces pipes, reservoirs, or desalination, it still matters if it can help solve specific water problems in specific places.

That is what makes this category one to look into.

Not because it will become the new default water infrastructure. It probably won’t. But because the world clearly needs more resilient and decentralized ways to produce or secure water where the traditional systems are not enough. Sometimes a technology does not need to solve everything to matter. It only needs to solve one painful problem well enough.

That was the path that got me into reading about AirJoule.

A simple way to think about the technology

The broader category is usually called atmospheric water generation, or atmospheric water harvesting. In simple terms, it means taking humidity from the air and turning it into usable water.

Most traditional systems do this in a fairly intuitive way: they cool air down until water condenses, basically like a large dehumidifier. That is both impressive and frustrating.

It can work, but it tends to become energy-hungry exactly where water is needed most, especially in hot and dry regions. Many conventional systems also struggle economically outside humid climates. That is why this category makes more sense to me as an off-grid complement, not as a replacement for large-scale municipal water infrastructure.

Why AirJoule caught my attention

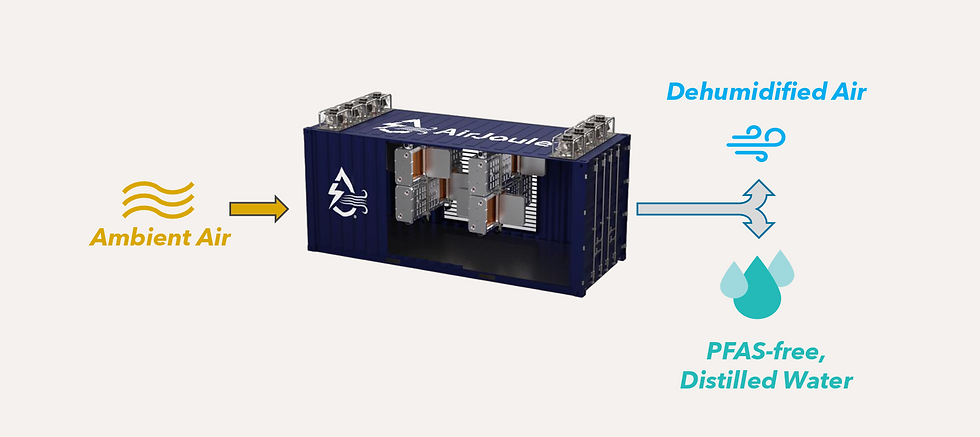

AirJoule is not pitching itself as just another giant dehumidifier. The company says its platform uses a sorbent-based process rather than brute-force cooling, combining advanced materials with a pressure-swing process and low-grade waste heat.

That is the part I find genuinely interesting.

The story here is not really, “Look, we can make water from nothing.” The more important story is that AirJoule seems to be trying to attack the hardest part of the problem: the economics.

If older atmospheric water systems were often limited by electricity usage and climate conditions, AirJoule’s angle is that waste heat may change the math. That matters because waste heat is everywhere in industry. It is especially relevant in data centers, which already consume enormous amounts of energy and, in many cases, large amounts of water for cooling.

AirJoule also talks about Water Purchase Agreements, where customers buy water by volume while AirJoule owns and operates the systems. That is a much more ambitious model than simply selling hardware.

Where the investing story gets harder

This is exactly where the investing story becomes harder than the technology story. Because this is where deep tech usually becomes a test of patience, capital, execution, and reality.

A compelling technical concept is one thing. A repeatable business is another. That distinction matters a lot.

AirJoule’s stock is down roughly a third year to date. That does not mean the market thinks the technology is worthless. It means the market wants more clarity on commercialization, timing, and real-world proof. And honestly, that seems fair.

The company says 2026 is supposed to be a transformational year as it moves from development to commercial deployment. It has a roadmap. It has partnerships. It has a story.

But the market is basically saying: now prove it.

So the story is not, “they have no plan.” The story is, “they still have to prove the plan.”

A personal reminder I carry with me

I learned this lesson the hard way before. Years ago, I bought shares in SolarWindow Technologies, a company developing electricity-generating glass for buildings. I loved the idea. I still love the idea. But loving the idea was not enough.

I sold my shares in 2022 at around a 60% loss. Painful, but still much better than what would have happened if I had simply held on. If I had kept holding, I would be down far more. The technology remained fascinating. The investment did not work for me.

That memory stayed with me while reading about AirJoule. It is very easy to confuse “this should exist” with “this will become a successful public company.” Those are not the same thing.

Strong names help, but they are not the answer

There are parts of the AirJoule story that look stronger than the average speculative climate-tech company. The company has meaningful industrial relationships around it. Its materials point to names like GE Vernova, Carrier, BASF, and the Net Zero Innovation Hub ecosystem. In Europe, it is working with a consortium that includes serious global players. That matters.

But serious names around a company are not the same as durable economics inside a company. That is the real investing gap. The biggest question is not whether the science is exciting. It is whether the system can perform reliably in dirty, inconsistent, real-world conditions for long enough to make the business model work.

Can the materials keep doing their job after many cycles?

Can the system deliver the promised economics outside a controlled setting?

Can a pilot become a repeatable product?

Can a product become a recurring contract?

Can a recurring contract become a durable business?

Those are very different stages. Public markets often compress them into one narrative. Real life does not.

Why this also feels personal to me as an Israeli

There is also another reason this topic resonates with me. As an Israeli, I immediately noticed that this is a domain where Israeli companies and institutions have already built real credibility.

Watergen has been pushing atmospheric water systems globally for years. The Technion has also highlighted atmospheric water technologies aimed at extracting water in arid and desert conditions.

That does not mean all these companies will win. But it does mean this is not a fantasy category with no real engineering behind it. There is already serious work here, including in Israel. That makes the space more interesting to follow.

What would a moat even look like here?

And that brings me to the moat question. This is not a classic moat business today. At least not yet. If a moat emerges in this space, it probably will not come from the broad idea of “water from air.” That idea is too open, too visible, and too attractive.

A real moat here would have to come from a much harder combination:

proprietary process know-how

material performance that holds up in the field

manufacturing capability

trusted commercial channels

customer integration

and years of operating data that help one company deliver better economics than everyone else

In other words, the moat would look less like a patent framed on a wall and more like a system that actually works better, lasts longer, and is easier to deploy at scale than alternatives.

It would also help if the business model creates recurring relationships, not just one-time hardware sales. That is what makes AirJoule’s Water Purchase Agreement idea interesting.

But interesting is not the same as proven.

My take

I think the need is obvious. Water stress is real. Climate pressure is real. Population growth and industrial demand are real. This category is worth paying attention to. The technology is fascinating. Not because it sounds futuristic, but because it seems to attack a real bottleneck in the economics of atmospheric water. I also think the market is behaving rationally by demanding more proof.

AirJoule may turn out to be an important company in this space. It may also turn out to be another example of a brilliant idea that takes much longer to commercialize than investors hope. That is the tension here. There is a big difference between a technology that deserves to exist and a stock that deserves your capital today.

Sometimes the opportunity is real, but still early. Sometimes the vision is right, but the timing is wrong.Sometimes the technology wins, but current shareholders do not.

And sometimes FOMO is what pushes investors to act too early.

That is why one of the hardest investing lessons is also one of the simplest: it is usually better to join later and safer than to join early just because the story is exciting. Missing part of the ride is often much better than being there for the wrong stretch of it.

AirJoule is on my watchlist for exactly that reason. Not because I think the story is simple.

Because it isn’t.